- April 1, 2025

Insurance in Superannuation – Default Insurance Cost Comparison

Damian Thornley | Partner | January-2025

Since 2021, Azuria Partners has been researching the competitiveness of the default insurance offerings by seven large public offer superannuation funds. This study is unique in the Australian market for its focus on the member default insurance packages.

In this report, we assess the following aspects of default insurance arrangements and their changes over time:

- Sum insured: Coverage for Death and Total and Permanent Disablement (TPD) benefits

- Annual premium: Cost of the default insurance cover, and

- “Value for customer”: Competitiveness of the premium rate per $1,000, highlighting improvements or declines in value.

To evaluate the market positioning of default insurance offerings, we reviewed the insurance guides of the following superannuation funds as of December 2024. Collectively, these funds account for over half of all superannuation fund members across Australia’s 100+ funds, underscoring their industry dominance and significance.

- AustralianSuper

- Hostplus

- Australian Retirement Trust (ART)

- Rest Super

- HESTA

- Aware Super

- Cbus Super

Key Themes / January-2025 Default Insurance Outcomes

- During 2024 a second major superannuation fund has moved to adopt Female / Male rating factors into their default insurance premium.

- Hostplus has moved to a Female / Male insurance premium structure.

- This is viewed as a positive market development. It is the second major fund to move away from unisex rates.

- If female risk factors are lower, this benefit should be passed on to females in their premium rate.

- Age-based premium rates are generally decreasing with an observed 5% rate improvement compared to our survey 18 months prior, in mid-2023.

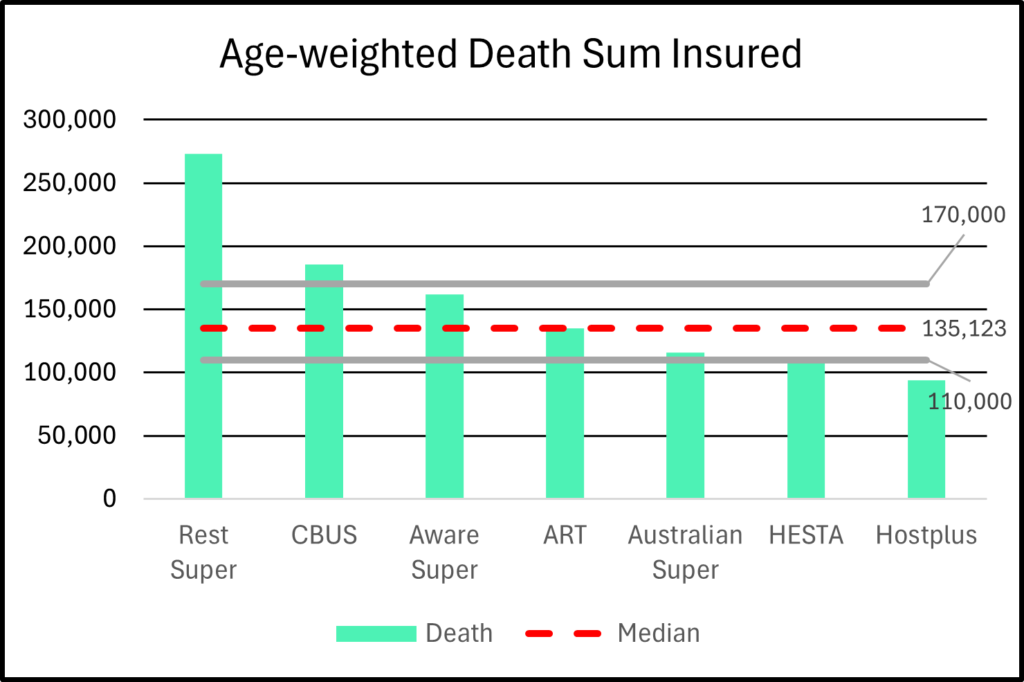

- Cover levels have been stable with no major changes. The median cover level for death insurance is $135,000 – which is noted to be low compared to average mortgage balance.

Key Themes in Superannuation Insurance

Our research has uncovered several critical insights into the default insurance offerings across major Australian Superannuation funds.

| Cover Levels | The weighted average death cover is reasonably comparable across most funds surveyed, ranging from $110,000 to $170,000. Rest Super is an outlier with higher levels of cover. The typical level of death cover ($135K) falls far short of the average new mortgage balance of $640,000 as reported by the ABS in September 2024. |

| Annual premiums spend | The annual premium charged by these funds for the default insurance package is close to:

These premiums are well below the industry guideline of 1% of salary, as highlighted in ASIC report 760 (2023), to prevent the erosion of superannuation balances due to insurance costs. |

| Competitiveness of Death & TPD rates per $1,000 sum insured | Hostplus (Female rates) has the lowest weighted Death & TPD premium rates per $1,000 sum insured, after its shift from unisex rates to gender specific rates. Five out of the seven funds surveyed continue to use unisex rates therefore blending the different risk ratings that naturally apply to Female / Male. ART (formerly Sunsuper) continues to use Female / Male rates, while Hostplus has transitioned from a unisex structure to Female / Male rates. This transition reflects Hostplus’s recognition of differing experiences between male and female members. |

Age-weighted Sum Insured | January-2025 results

Figure 1 – Age-weighted cover levels by super fund for death cover

Figure 1: Rest Super and Cbus Super offer the largest death cover coverages, exceeding the median by 102% and 37%, respectively.

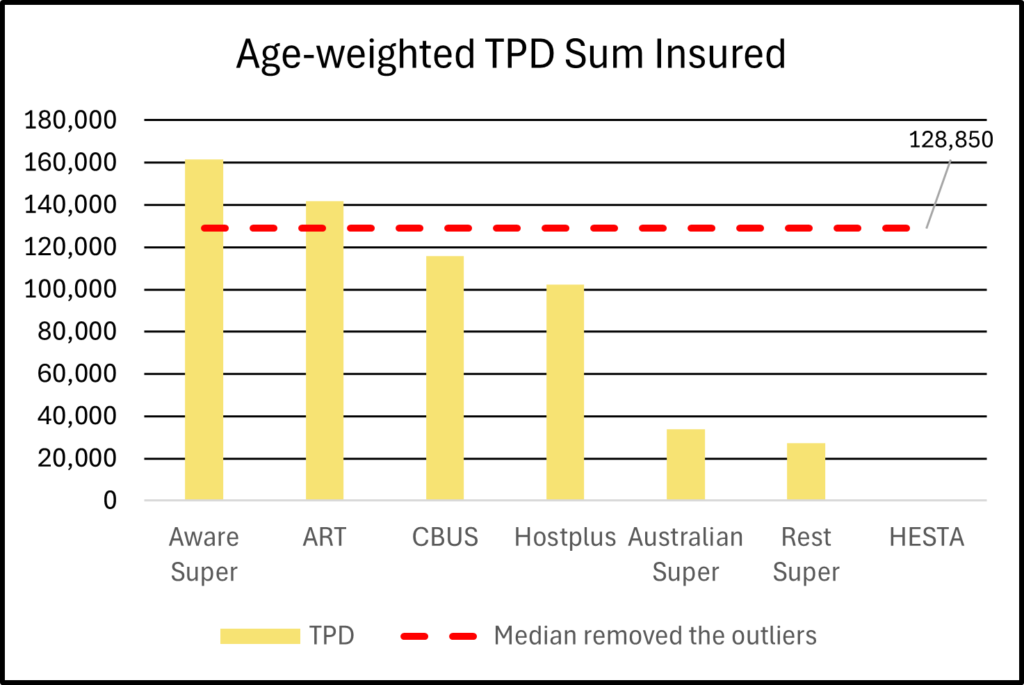

This is likely due to their focus on high-risk professions, where higher death cover is designed to meet the specific needs of their members. Four of the seven funds (Aware Super, ART, AustralianSuper, HESTA) offer average death cover between $110,000 and $170,000, highlighting the consistency of death benefits across the major funds.Figure 2 – Age-weighted cover levels by super fund for TPD cover

Figure 2: Aware Super and ART currently offer the highest coverage for TPD.

AustralianSuper, Rest Super, and HESTA provide income protection, which explains their lower TPD values.

The variance suggests that each fund adjusts its TPD coverage to balance comprehensive protection and financial sustainability.

HESTA does not provide default insurance for TPD.

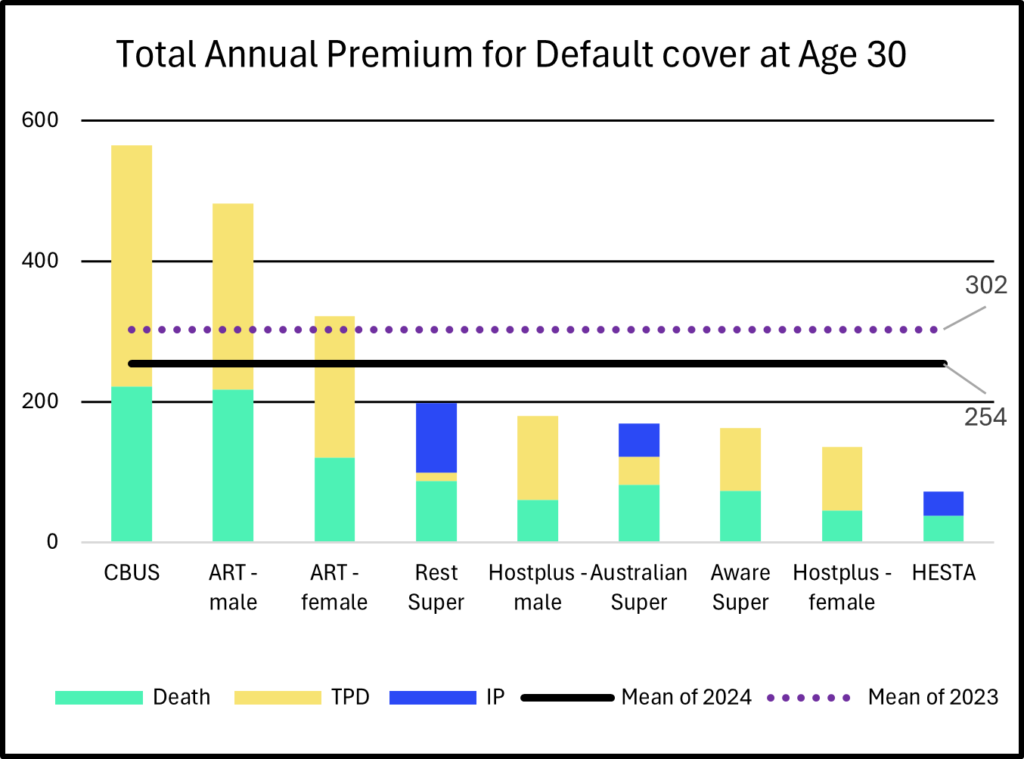

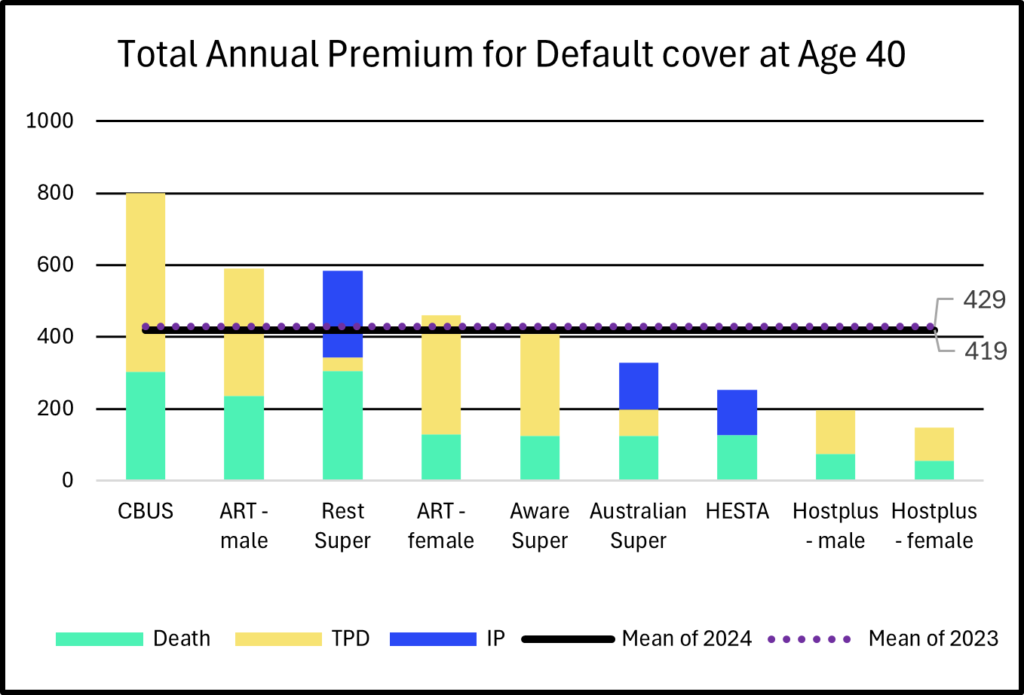

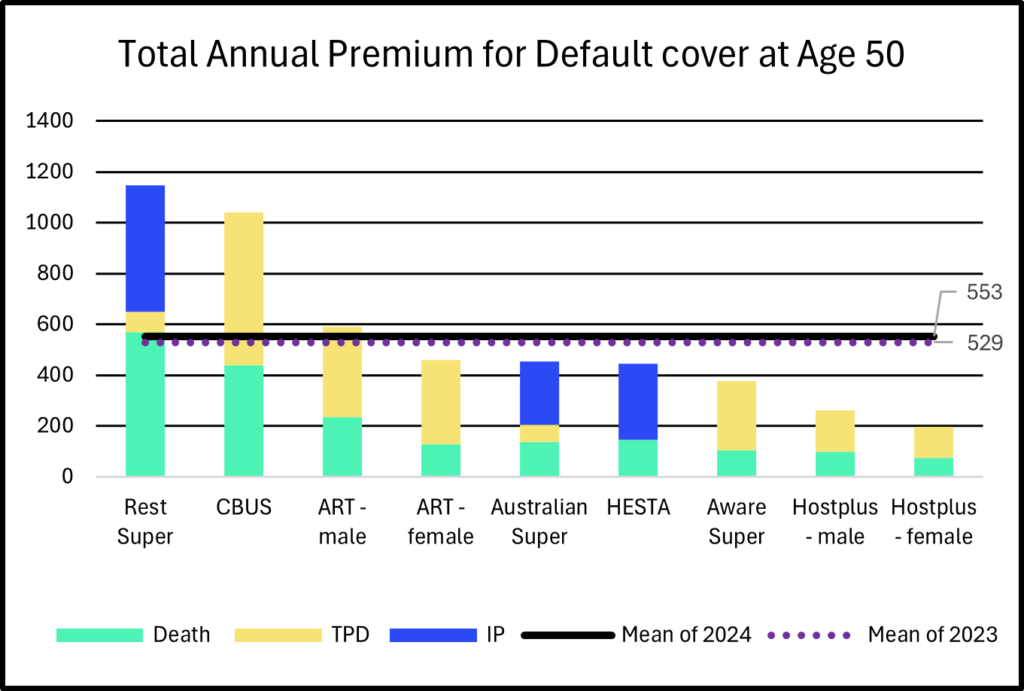

Total Annual Premium | January-2025 results

The mean default insurance premiums range from $200 to $600 per annum for individuals aged 30-50. This is within the recommended guideline of 1% of salary for maximum insurance premiums. We generally observed some reduction in the annual premium at younger ages.

Figure 3: Total Annual premiums for ages 30,40 and 50

Within the 30-40 age bands: Cbus Super remains the most expensive in total annual premiums. This is likely due to the occupational & gender balance of the membership.

At age band 40:

- Average annual premium at age 40 is just over $400pa.

- The average total annual premium remains relatively stable compared to 2023 report.

Overall trend:

The mean premium decreases by 16% at age 30, 2% at age 40, and increases by 5% at age 50.

This may be an effort to reduce cross-subsidisation, making premiums fairer by lowering costs for younger members.

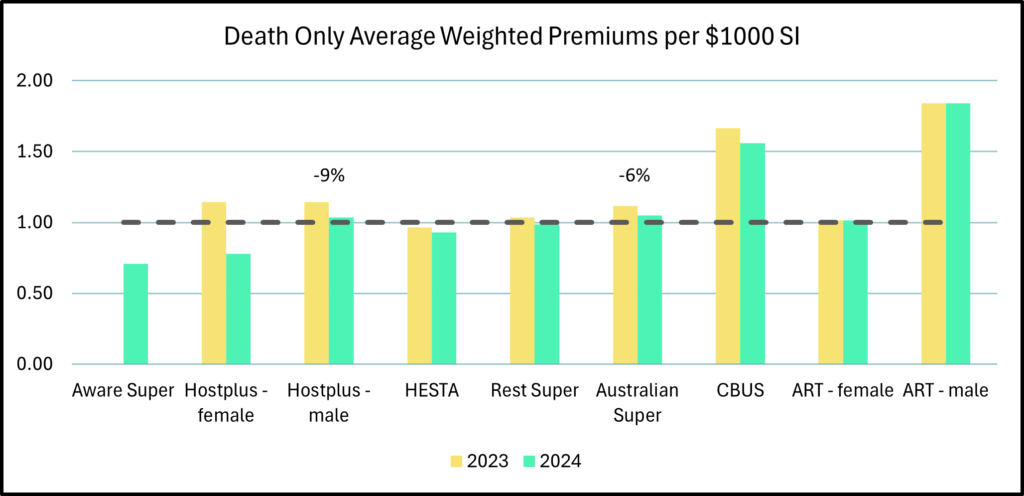

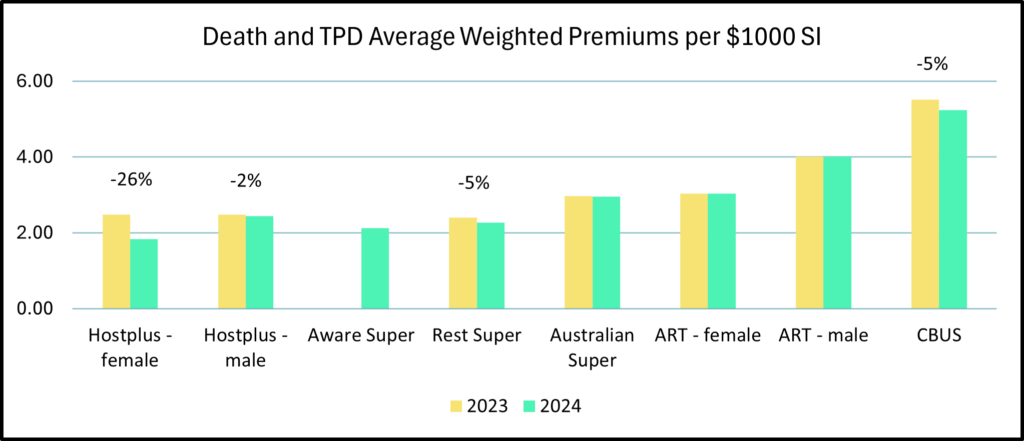

Average weighted premiums per $1000 of cover – value to the customers | January-2025 results

Figure 4: Weighted average underlying premiums for death coverage

Figure 5: Weighted average underlying premiums for Death and TPD coverage

- Figure 4 illustrates that four funds have weighted annual death premiums below $1 per $1000. Aware[1] Super is the most competitive, followed by Hostplus (female), HESTA and Rest Super.

- Figure 5 shows that Hostplus, Rest Super and Cbus Super have become more competitive over the last year, with decreases in premium of 26% (Hostplus female), 2% (Hostplus male), 5% for Rest Super and Cbus Super.

- Hostplus has revised its structure to align with gender-based pricing.

- Overall, the total death and TPD average-weighted annual premium of the seven funds decreased by 5% compared to mid-2023.

___________________________________

1See Appendix: Methodology for details on the age-weighted method.

2Median of TPD cover has been calculated using only four largest funds to eliminate outlier effects.

3HESTA does not offer default TPD cover, thus there is no comparability to other funds.

4 Aware Super has modified its structure of default offerings. Thus, there is no comparability to previous years, however inferences can be made by comparing across all funds.

Conclusion

Default annual insurance premiums exhibit a decreasing trend, with average death and TPD premiums declining for younger age bands. For members aged 50, premiums remain relatively stable but show slight increases. For members aged 30-50, premiums consistently range between $200 and $600 per annum.

Notable changes include adjustments to premium structures, such as age-weighted and gender-based pricing, reflecting a shift towards more tailored and competitive insurance offerings. Premium trends reveal a general decrease for younger age groups, while older members experience stable or slightly increasing premiums due to higher coverage needs.

Moving forward, it is crucial for superannuation funds to continue monitoring and adjusting their insurance offering to meet the evolving needs of their members, by maintaining affordability and enhancing value for money.

Appedix

Scope clarification

Default Income Protection has been excluded from the analysis in this report.

Methodology

In the analysis, we surveyed each superannuation funds Insurance Guide to collect detailed data on default insurance premiums, cover levels. To ensure comparability of our analysis across funds, we applied a weighted average approach. This approach involves weighting cover levels and sums insured according to age distribution within the labour force. This method allowed us to compare better across fund offerings, thereby providing a comprehensive view of the insurance landscape.