- May 21, 2026

How has increased scrutiny by regulators affected Life Insurance premium changes?

May-2026

Since December 2022, Australian Prudential Regulation Authority (APRA) and Australian Securities and Investments Commission (ASIC) have conducted a joint review regarding concerns about frequent and unexpected premium increases in retail life insurance products. This review was followed up in December 2023 with a letter of expectation and a further review in 2025 following an implementation period.

Although the review was conducted and released jointly, the regulators’ observations reflected ASIC’s traditional focus on consumer disclosure and marketing practices, alongside APRA’s emphasis on product sustainability, governance, and long-term premium stability. Regulators were particularly concerned about policies marketed using the term “level premiums”, where premium increases often appeared inconsistent with consumer expectations regarding long-term price stability.

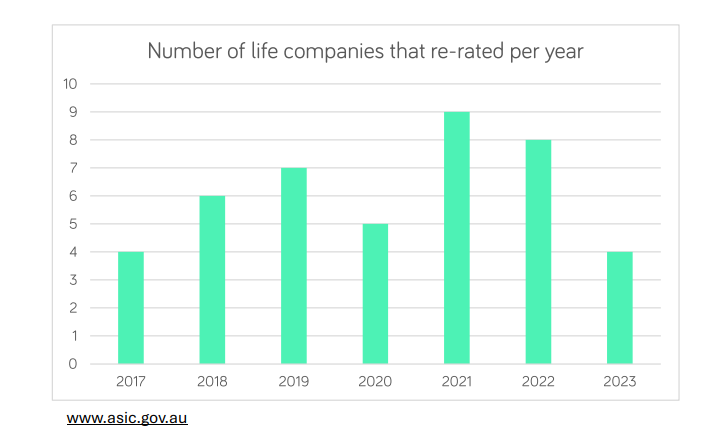

Between 2017 and 2023, 13 of the 16 life insurers offering retail life insurance products re-rated at least once, while 7 insurers re-rated four or more times. These repeated adjustments raised concerns about transparency, fairness, and whether policyholders fully understood the circumstances under which premiums could increase.

Regulatory Response

In December 2023, APRA and ASIC reaffirmed their concerns regarding misleading premium disclosures and set several expectations for life insurers. These included:

- Ensuring strong risk management and compliance frameworks around re-rating practices.

- Ensuring policy terms allowing premium increases were transparent and fair.

- Clearly explaining how premiums are calculated and how they may change over time; and

- Designing products with greater consideration for long-term premium stability.

The regulators also encouraged insurers to reconsider the design of future products. This included improving product sustainability, reducing the likelihood of sharp premium increases, and ensuring premium terminology accurately reflected how products behaved in practice.

As part of these reforms, insurers were given 12 months to update premium terminology and disclosure practices. Consequently, policies issued after 31 December 2024 were required to adopt the labels “variable” and “variable age-stepped” rather than “level” premiums.

Where Are We Now?

In June 2025, APRA and ASIC released a follow-up review where they address how effectively life insurers1 had responded to earlier regulatory expectations and set future expectations2.

The regulators concluded that the industry has made meaningful but incomplete progress. Insurers have improved governance processes, strengthened disclosure practices, and reviewed re-rating procedures. However, ASIC and APRA noted that many of these changes were still relatively recent, making it difficult to determine whether they would meaningfully improve long-term consumer outcomes or reduce premium volatility, stating “it is too early to determine whether the changes implemented by life companies will improve long-term consumer outcomes.” And “significant work remains to improve premium stability and consumer understanding.”

Changes Following the 2025 Update

| Area | Before Review (Pre-2022) | After Review (2025 Update) |

| Re-rating Practices: | Unclear contractual rights, weak controls | Improved governance, contract reviews, and customer refunds |

| Premium Labels | “Level” vs “Stepped” | “Variable” and “Variable age-stepped” |

| Consumer Understanding | Misconceptions about stability | Improved disclosures & projections |

| Product Governance | Limited focus on long-term outcomes | Stronger Target Market Determinations and governance frameworks |

| Premium Stability | High volatility, unexpected increases | Ongoing concern; not yet fully resolved |

ASIC and APRA found that the issues identified in earlier reviews were widespread across the industry and have materially affected consumers. A major concern remains the disconnect between consumer expectations and the actual behaviour of products marketed as providing “level” premiums.

Many consumers did not fully understand how premiums could change over time, partly due to unclear disclosure and misleading terminology. In response, several insurers implemented corrective measures, including:

- Refunding premiums where increases were not contractually justified.

- Revising policy wording and disclosure documents.

- Improving marketing materials; and

- Strengthening governance and oversight processes.

Despite these improvements, regulators stated that structural issues remain within premium design and pricing models. In particular, duration-based pricing structures and heavy reliance on introductory discounts continue to contribute to premium volatility over the life of a policy. ASIC and APRA observed that:

“In response to our joint review, a few life companies launched products in the past year that appear to better promote sustainability and premium stability. However, product innovation across the industry is still limited.”

Future Expectations for Life Insurers

Going forward, APRA and ASIC expect insurers to place greater emphasis on sustainability, transparency, and long-term consumer outcomes.

This includes:

- Designing products that provide more stable premiums over time.

- Clearly communicating the potential for future premium increases.

- Improving explanations of pricing structures, including discounts and duration-based pricing; and

- Providing stronger support for customers experiencing affordability pressures following premium increases.

Regulators also emphasised that insurers must move beyond short-term compliance responses and instead embed consumer-focused thinking into product design and governance practices. Ultimately, ASIC and APRA expect life insurance products to be sustainable, transparent, and aligned with the long-term interests of policyholders rather than relying on reactive pricing adjustments.

1APRA & ASIC, Addressing premium increases in life insurance products (2023).

2APRA & ASIC, Premium increases in life insurance: Are life companies addressing issues identified by

regulators? (2025)